Posted on

January 25, 2022

by

Team Jillain

TOP CONSIDERATIONS FOR 2022:

COVID-19 IMPACTS ON ECONOMY AND INFLATION- Supply disruptions caused by COVID-19 are expected to ease in 2022. However, if new variants emerge that delay a full re-opening, this could impact the economic recovery, while prolonging supply challenges and inflationary pressure.

LENDING- The Bank of Canada is expected to increase interest rates in 2022. While gradual gains are anticipated, rates are expected to remain below pre-pandemic levels – low enough to continue to support housing demand, but not at the pace seen in 2021.

POPULATION- The flow of migration will be an important component of sustaining high levels of demand in housing markets.

HOUSING SUPPLY- New construction and elevated levels of listings in the resale market are expected to help add to the undersupplied housing market. The spring market is expected to remain relatively tight, but if supply levels do not start to improve in the second half of the year, this will have significant implications for home prices.

It will take time for the housing market to move out of sellers’ conditions, supporting further price gains this year.

EMPLOYMENT

Following the dramatic decline in jobs in 2020, it is not a surprise that employment levels increased by over four per cent in 2021. Employment gains since September, in particular, were exceptionally strong in Calgary. As of December, employment levels pushed above 833,000, higher than pre-pandemic levels and just shy of peak employment that occurred in June 2019.

Job growth occurred for both full- and part-time positions across a wide range of industries. As of December 2021, sectors such as construction; wholesale and retail trade; finance, insurance and real estate; and professional and technical services not only recovered from the start of the pandemic, but soared to near or above previous highs in the market. These improvements, especially in the professional and technical services sector, will help support further demand growth in the housing market.

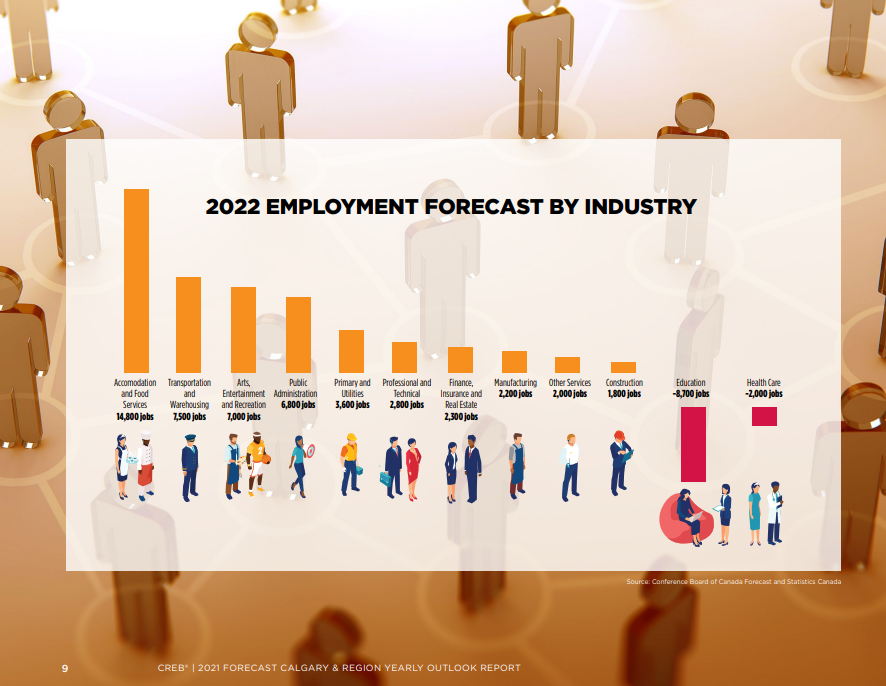

Employment gains are expected to continue into 2022, with annual gains forecasted to rise by nearly five per cent. With COVID-19 expected to be mostly behind us, the largest gains in jobs are expected in some of the hardest hit areas, including accommodation and food; arts, entertainment and recreation; and transportation and warehousing. Further gains are also expected in some of our higherpaying industries, including the primary, utilities and manufacturing sectors. The only sector expected to see additional pullback is educational services.

Unemployment rates are also expected to trend down, but to levels that remain higher than pre-pandemic levels. This is, in part, due to gains in the labour force, as more people re-enter the job market. This could also be related to some of the concerns regarding the mismatch between job seekers and job availability.

Some sectors have been struggling to find qualified workers despite higher unemployment levels, somewhat evidenced by rising job vacancy rates. The mismatch would likely also create divergent trends in wages, with sectors experiencing high job vacancies seeing steeper wage growth relative to other sectors. To date, wages have been generally trending up, but not necessarily at the same pace as inflation, impacting growth in disposable income in 2021. As we move into 2022, wages are expected to rise, supporting gains in household income.

Please read the full forecast here.